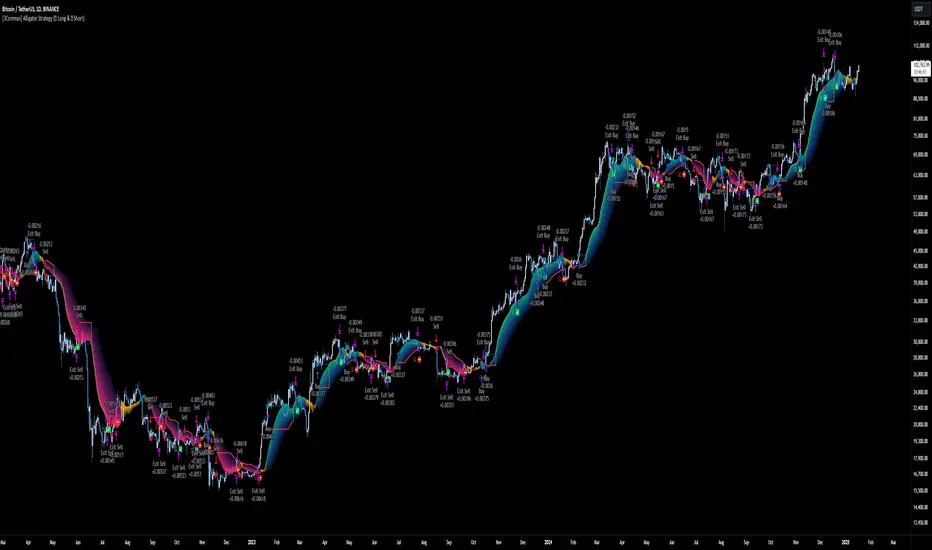

[3Commas] Alligator StrategyThe Alligator Strategy

🔷 What it does: This script implements the Alligator Strategy, a trend-following method created by Bill Williams. It uses three customizable moving averages (SMMAs or RMAs) "Jaws," "Teeth," and "Lips" to identify market trends and potential trade opportunities. Additionally, it includes built-in stop-loss and take-profit options for enhanced risk management.

🔷 Who is it for:

Trend Traders: Those who prefer trading in markets with clear directional movement.

Advanced Users: Traders who require customizable tools and dynamic risk management features.

Beginners: Accessible to those new to trading, thanks to its intuitive visual representation of trends and pre-configured settings.

Bot Users: Supports direct signal integration for bot automation, including entries, take-profits, and stop-losses.

🔷 How does it work: The Alligator Jaws, Teeth, and Lips are smoothed moving averages (SMA, EMA, RMA, or WMA) calculated based on the selected source price ( hl2 = (high+low)/2 by default). Their lengths and offsets are customizable:

Jaws: Length 21 , offset 13.

Teeth: Length 13, offset 8.

Lips: Length 8 , offset 5.

When the lines align and spread apart (e.g., Lips > Teeth > Jaws for an uptrend), the strategy identifies a trending market.

Entry Conditions:

Long Trades: Triggered when Close > Lips > Teeth > Jaws.

Short Trades: Triggered when Close < Lips < Teeth < Jaws.

🔷 Why it’s unique:

Customization: Flexible settings for moving average types and lengths to adapt to different market conditions and strategy tester configurations.

Built-in Filters: Trend filters that can reduce false signals in certain scenarios, making it more reliable for trending markets.

Take Profit and Stop Loss:

Configurable as either percentage-based or dynamic.

Stop-loss levels adjust dynamically using the Alligator lines.

Fast exit logic moves the stop-loss closer to the price when trades are in profit.

3Commas Bot Compatibility: Designed for automated trading, allowing traders to configure and execute the strategy seamlessly.

🔷 Considerations Before Using the Indicator

🔸Why the Forward Offset: By shifting the averages forward, the Alligator helps traders focus on established trends while filtering out short-term market noise.

The standard configurations of 13-8, 8-5, and 5-3 were selected based on Bill Williams’ studies of market behavior. However, these values can be adjusted to suit different market conditions:

Volatile Markets: Faster settings (e.g., 10-6, 6-4, 3-2) may provide earlier signals.

Less Volatile Markets: Slower settings (e.g., 21-13, 13-8, 8-5) can help avoid noise and reduce false signals.

🔸Best Timeframes to Use: The Alligator can be applied across all timeframes, but certain timeframes offer better reliability.

Higher Timeframes (H4, D1, W1): Ideal for identifying significant trends and for swing or position trading.

Lower Timeframes: Not recommended due to increased noise but may work for scalping with additional confirmation tools.

🔸Disadvantages of the Alligator Strategy:

Exhausted Entry Levels: High buying levels or low selling levels can lead to momentum exhaustion and potential pullbacks.

False Signals in Ranges: Consolidating markets can produce unreliable signals.

Lagging Indicator: As it is based on moving averages, it may delay reacting to sudden price changes.

🔸Advantages of the Alligator Strategy:

Trend Focused: Simplifies the identification of trending markets.

Noise Reduction: Forward shifts and smoothed averages help filter out short-term price fluctuations.

Broad Applicability: Suitable for forex, crypto, stocks, and commodities.

🔸Important Considerations:

While the Alligator Strategy provides a systematic way to analyze markets, it does not guarantee successful outcomes. Results in trading depend on multiple factors, including market conditions, trader discipline, and risk management. Past performance of the strategy does not ensure future success, and traders should always approach the market with caution.

Risk Management: Define stop-loss levels, position size, and profit targets before entering any trade. Be prepared for the possibility of losses and ensure that your approach aligns with your overall trading plan.

🔷 STRATEGY PROPERTIES

Symbol: BINANCE:BTCUSDT (Spot).

Timeframe: 1D (Daily Timeframe).

Test Period: All historical data available.

Initial Capital: 10000 USDT.

Order Size per Trade: 1% of Capital, you can use a higher value e.g. 5%, be cautious that the Max Drawdown does not exceed 10%, as it would indicate a very risky trading approach.

Commission: Binance commission 0.1%, adjust according to the exchange being used, lower numbers will generate unrealistic results. By using low values e.g. 5%, it allows us to adapt over time and check the functioning of the strategy.

Slippage: 5 ticks, for pairs with low liquidity or very large orders, this number should be increased as the order may not be filled at the desired level.

Margin for Long and Short Positions: 100%.

Indicator Settings: Default Configuration.

Alligator: Source hl2 | Calculation RMA | Jaw 21-13, Teeth 13-8, Lips 8-5.

Strategy: Long & Short.

Max Stop Loss per Trade: 10% of Trade Size.

Exit trades on opposite signal: Enable.

Alligator Stop Loss: Enable.

Alligator Fast Exit: Enable.

🔷 STRATEGY RESULTS

⚠️ Remember, past results do not guarantee future performance.

Net Profit: +355.68 USDT (+3.56%).

Total Closed Trades: 103.

Percent Profitable: 47.57%.

Profit Factor: 1.927.

Max Drawdown: -57.99 USDT (-0.56%).

Average Trade: +3.45 USDT (+3.41%).

Average # Bars in Trades: 16.

🔷 HOW TO USE

🔸Adjust the Alligator Settings:

The default values generally work well: Source hl2 | Calculation RMA | Jaw 21-13, Teeth 13-8, Lips 8-5. However, if you want to use it on timeframes smaller than 4H (4 hours), consider increasing the values to better filter market noise.

Please review the "Indicator Settings" section for configuration.

🔸Choose a Symbol that Typically Trends:

Select an asset that tends to create trends. However, the Strategy Tester results may display poor performance, making it less suitable for sending signals to bots.

🔸Add Trend Filters:

You can enable trend filters like MA and SuperTrend. By default, these are disabled as they are often unnecessary, but you can experiment with their configuration to see if they optimize the strategy's results.

Please review the "Indicator Settings" section for configuration.

🔸Enable Stop Loss Levels:

Activate Stop Loss features, such as Stop Loss % or Alligator Stop Loss. If both are enabled, the one closest to the price during the trade will be applied.

Please review the "Indicator Settings" section for configuration.

🔸Enable Take Profit Levels:

Activate Take Profit options, such as Take Profit % or Alligator Fast Exit. If both are enabled, the one that triggers first will be executed.

Please review the "Indicator Settings" section for configuration.

This is an example with the default settings and how Alligator Stop Loss and Alligator Fast Exit are activated:

In this example, we additionally enable the Take Profit at 10%. We can observe that the Alligator Stop Loss is the active one since it is closer to the price. When the price moves 10% in favor or against the trade, the position is closed. Although the Alligator Fast Exit is enabled, it does not activate because the trades are closed beforehand.

🔸Results Review:

It is important to check the Max Drawdown. This value should ideally not exceed 10% of your capital. Consider adjusting the trade size to ensure this threshold is not surpassed.

Remember to include the correct values for commission and slippage according to the symbol and exchange where you are conducting the tests. Otherwise, the results will not be realistic.

If you are satisfied with the results, you may consider automating your trades. However, it is strongly recommended to use a small amount of capital or a demo account to test proper execution before committing real funds.

🔸Create alerts to trigger the DCA Bot

Verify Messages: Ensure the message matches the one specified by the DCA Bot.

Multi-Pair Configuration: For multi-pair setups, enable the option to add the symbol in the correct format.

Signal Settings: Enable whether you want to receive long or short signals (Entry | TP | SL), copy and paste the the messages for the DCA Bots configured in 3Commas.

Alert Setup:

When creating an alert, set the condition to the indicator and choose "alert() function call only.

Enter any desired Alert Name.

Open the Notifications tab, enable Webhook URL, and paste the Webhook URL from 3Commas.

For more details, refer to the 3Commas section: "How to use TradingView Custom Signals.

Finalize Alerts: Click Create, you're done! Alerts will now be sent automatically in the correct format to 3Commas.

🔷 INDICATOR SETTINGS

🔸Alligator Settings

MA's source: Source price for Alligator moving averages.

MA's Type: Type of calculation for MA's.

Jaw and Offset: Jaw length and offset to the right.

Teeth and Offset: Teethlength and offset to the right.

Lips and Offset: Lips length and offset to the right.

🔸Alligator Style

Plot Alligator: Show Alligator Ribbon.

Plot MA's: Show Alligator MA's.

Colors: Main and Gradient Colors for Bullish Alligator, Berish Alligator, Neutral Alligator. For gradient colors it is recommended to use an opacity of 15.

🔸MA & SuperTrend Filters

MA & Plot: Activate MA Filter and Plot MA on the chart.

Long Entries: When activated, it will only execute entries if the price is above the MA

Short Entries: When activated, it will only execute entries if the price is below the MA.

Source: Source price for moving average calculations.

Length: Candles to be used by the MA calculations.

Type: Type of calculation for MA.

Timeframe: Here you can select a larger timeframe for the filter.

ST & Plot: Activate SuperTrend Filter and Plot SuperTrend on the chart.

Long Entries: When activated, it will only execute entries if the price is above the SuperTrend.

Short Entries: When activated, it will only execute entries if the price is below the SuperTrend.

Source: Source price for SuperTrend calculations.

Length: Candles to be used by the SuperTrend calculations.

Factor: ATR multiplier of the SuperTrend.

Timeframe: Here you can select a larger timeframe for the filter.

🔸Strategy Tester

Strategy: Order Type direction in which trades are executed.

Take Profit %: When activated, the entered value will be used as the Take Profit in percentage from the entry price level.

Stop Loss %: When activated, the entered value will be used as the Stop Loss in percentage from the entry price level. If Alligator Stop Loss is activated, the closest one to the price will be used.

Exit trades on opposite signal: This option closes the trade if the opposite condition is met. For instance, if we are in a long position and a sell signal is triggered, the long position will be closed, and a short position will be opened. The same applies inversely.

Alligator Stop Loss: In a long trade, the lower part of the Alligator indicator will be used as a dynamic stop loss. Similarly, in a short trade, the upper part of the indicator will be used.

Alligator Fast Exit: Its purpose is to attempt to protect movements in favor of the trade's direction. In the case of long trades, once the price and the upper part of the Alligator indicator are above the trade's entry price, the stop loss will be moved to the upper part. For short trades, once the price and the lower part of the Alligator indicator are below the trade's entry price, the stop loss will be moved to the lower part of the Alligator indicator.

Alligator Squeeze Entry: When activated, entries will only be executed if they meet the condition after a neutral zone of the Alligator indicator.

Alligator Squeeze Exit: When this option is activated, any open trades will be closed when the Alligator indicator enters a neutral mode.

Use Custom Test Period: When enabled signals only works in the selected time window. If disabled it will use all historical data available on the chart.

Test Start and End: Once the Custom Test Period is enabled, here you select the start and end date that you want to analyze.

🔸3Commas DCA Bot Signals

Check Messages: Enable the table to review the messages to be sent to the bot.

Entry | TP | SL: Enable this options to send Buy Entry, Take Profit (TP), and Stop Loss (SL) signals to 3Commas.

Deal Entry and Deal Exit : Copy and paste the message for the deal start signal and close order at Market Price of the DCA Bot you created in 3Commas. This is the message that will be sent with the alert to the Bot, you must verify that it is the same as the 3Commas bot so that it can process properly so that it executes and starts the trade.

DCA Bot Multi-Pair: You must activate it if you want to use the signals in a DCA Bot Multi-pair in the text box you must enter (using the 3Commas format) the symbol in which you are creating the alert, you can check the format of each symbol when you create the bot.

🔷 CONCLUSION

The Alligator Strategy is a valuable tool for identifying potential trends and improving decision-making. However, no trading strategy is foolproof. Careful consideration of market conditions, proper risk management, and personal trading goals are essential. Use the Alligator as part of a broader trading system, and remember that consistent learning and discipline are key to success in trading.

👨🏻💻💭 We hope this tool helps enhance your trading. Your feedback is invaluable, so feel free to share any suggestions for improvements or new features you'd like to see implemented.

____________________________________________________________________

The information and publications within the 3Commas TradingView account are not meant to be and do not constitute financial, investment, trading, or other types of advice or recommendations supplied or endorsed by 3Commas and any of the parties acting on behalf of 3Commas, including its employees, contractors, ambassadors, etc.

Cari dalam skrip untuk "the strat"

Smart DCA Invest LiteEnglish description:

📊 Smart DCA Invest – Features Overview

✅ Automated DCA strategy with dynamic profit targets, optimized risk management.

⚙️ Functionality:

🕒 Time Interval Settings

• 📅 Start Date and Time: The strategy activates only after the specified start time.

• 🔄 Auto Restart: Automatically restarts the strategy after a position is closed.

💵 Investment Amounts

• 🟢 Initial Investment Amount: The amount invested when the first position is opened.

• 🔄 Recurring Investment Amount: The amount invested periodically for subsequent purchases.

📊 Purchase Frequency

• ⏱ Interval Between Purchases: Specifies the minimum number of candles between two purchases to avoid overly frequent position expansions.

🛡️ Risk Management

• 📉 Loss Limit: The strategy halts additional purchases if the price does not drop below a predefined loss level, optimizing the average cost reduction.

• 🎯 Take Profit: A predefined profit target percentage, triggering position closure upon reaching it.

📈 Dynamic Take Profit (TP) Settings

• ⏳ TP Increase Frequency: The interval in days for dynamic TP growth.

• 📊 TP Growth Rate: The percentage by which the TP level increases at the end of each interval.

• ⚙️ Enable Dynamic TP: Allows the TP level to increase dynamically over time based on holding duration.

• 🧠 Smart Invest: Accumulates skipped purchases above the average entry or loss limit price and invests them when the price drops below the loss limit.

🎨 Visual Representation

• 📏 Average Price Line: Displays the average entry price in yellow.

• 🛑 Stop Limit Line: Displays the loss limit in red.

• ✅ Take Profit Line: Displays the dynamically updated profit target in green.

🎨 Visual Elements

• 📏 Average Price Line: Visualizes the average cost on the chart.

• 🛑 Stop Limit Line: Visualizes the loss limit level.

• ✅ Take Profit Line: Displays the TP level graphically.

• 📊 Statistics Table: Detailed data summary presented in a table at the end of the strategy.

📊 Statistics Table

• 📈 Average Price: The average entry price of the current position.

• 🛑 Stop Limit: The loss limit value.

• ✅ Take Profit: The profit target value.

• 📦 Position Size: The size of the current position.

• 💵 Max Invested Amount: The highest amount invested.

• ⏳ Longest DCA Period: The longest duration a DCA position was open.

• 💼 Current Investment: The amount currently invested.

• 🔄 Multiplier: Purchase multiplier value.

• 📊 Dynamically Adjusted TP %: The current dynamic Take Profit percentage.

- Recommended for retesting

Hungarian description:

📊 Smart DCA Invest – Funkciók Leírása

✅ Automatizált DCA stratégia dinamikus profitcélokkal, optimalizált kockázatkezeléssel.

⚙️ Működés:

🕒 Időintervallum Beállítások

• 📅 Kezdési dátum és idő: A stratégia csak a meghatározott kezdési időpont után aktiválódik.

• ⏳ Befejezési dátum és idő: A stratégia a meghatározott időpontig működik.

• 🔄 Automatikus újraindítás: Pozíciózárás után a stratégia automatikusan újraindulhat.

💵 Befektetési Összegek

• 🟢 Első befektetési összeg: Az első pozíció nyitásakor befektetett összeg.

• 🔄 Napi vásárlási összeg: Ismételt periódusonkénti vásárlások összege.

📊 Vásárlási Gyakoriság

• ⏱ Intervallum két vásárlás között: Meghatározza a minimális gyertya intervallumot két vásárlás között, elkerülve a túl gyakori pozícióbővítéseket.

🛡️ Kockázatkezelés

• 📉 Loss Limit: Ha az ár nem csökken egy meghatározott veszteségi szint alá, a stratégia nem vásárol tovább, hogy hatékonyabban csökkentse az átlagárat.

• 🎯 Take Profit: Előre meghatározott profitcél százalékos értéke, amely elérésekor a pozíció lezárul.

📈 Dinamikus Take Profit (TP) Beállítások

• ⏳ TP növelési gyakoriság: A dinamikus TP növekedésének időszaka napokban.

• 📊 TP növekedés mértéke: A TP szint százalékos növekedése az intervallum végén.

• ⚙️ Dinamikus TP engedélyezése: A TP szint dinamikusan növekszik a tartási idő függvényében.

• 🧠 Smart Invest: Kihagyott vásárlások felhalmozása (átlagos bekerülési vagy „Loss limit” feletti árfolyamnál), amelyek a „Loss limit” árszint alatt befektetésre kerülnek.

🎨 Vizuális Megjelenítés

• 📏 Átlagár vonal: Sárga színnel jelzi az átlagárat.

• 🛑 Stop Limit vonal: Piros színnel jelzi a veszteségi korlátot.

• ✅ Take Profit vonal: Zöld színnel jelzi a dinamikusan frissülő profitcélt.

🎨 Vizuális Elemek

• 📏 Átlagár vonal: Az átlagár megjelenítése a grafikonon.

• 🛑 Stop Limit vonal: A veszteségkorlátozási szint megjelenítése.

• ✅ Take Profit vonal: A Take Profit szint grafikai megjelenítése.

• 📊 Statisztikai táblázat megjelenítése: A stratégia végén részletes adatok jelennek meg egy táblázatban.

📊 Statisztikai Táblázat

• 📈 Átlagár: Az aktuális pozíció átlagos bekerülési ára.

• 🛑 Stop Limit: A veszteségkorlátozási szint értéke.

• ✅ Take Profit: A profitcél értéke.

• 📦 Pozícióméret: Az aktuális pozíció nagysága.

• 💵 Maximális befektetett összeg: A legnagyobb befektetett érték.

• ⏳ Leghosszabb DCA időszak: A leghosszabb időtartam, amíg egy DCA pozíció nyitva maradt.

• 💼 Aktuális befektetés: Az aktuálisan befektetett összeg.

• 🔄 Multiplikátor: Vásárlási szorzó érték.

• 📊 Dinamikusan beállított TP %: Az aktuálisan érvényes Take Profit százalékos értéke.

Bullish Reversal Bar Strategy [Skyrexio]Overview

Bullish Reversal Bar Strategy leverages the combination of candlestick pattern Bullish Reversal Bar (description in Methodology and Justification of Methodology), Williams Alligator indicator and Williams Fractals to create the high probability setups. Candlestick pattern is used for the entering into trade, while the combination of Williams Alligator and Fractals is used for the trend approximation as close condition. Strategy uses only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator or the candlestick pattern invalidation to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Trend Trade Filter: strategy uses Alligator and Fractal combination as high probability trend filter.

Methodology

The strategy opens long trade when the following price met the conditions:

1.Current candle's high shall be below the Williams Alligator's lines (Jaw, Lips, Teeth)(all details in "Justification of Methodology" paragraph)

2.Price shall create the candlestick pattern "Bullish Reversal Bar". Optionally if MFI and AO filters are enabled current candle shall have the decreasing AO and at least one of three recent bars shall have the squat state on the MFI (all details in "Justification of Methodology" paragraph)

3.If price breaks through the high of the candle marked as the "Bullish Reversal Bar" the long trade is open at the price one tick above the candle's high

4.Initial stop loss is placed at the Bullish Reversal Bar's candle's low

5.If price hit the Bullish Reversal Bar's low before hitting the entry price potential trade is cancelled

6.If trade is active and initial stop loss has not been hit, trade is closed when the combination of Alligator and Williams Fractals shall consider current trend change from upward to downward.

Strategy settings

In the inputs window user can setup strategy setting:

Enable MFI (if true trades are filtered using Market Facilitation Index (MFI) condition all details in "Justification of Methodology" paragraph), by default = false)

Enable AO (if true trades are filtered using Awesome Oscillator (AO) condition all details in "Justification of Methodology" paragraph), by default = false)

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. The first and key concept is the Bullish Reversal Bar candlestick pattern. This is just the single bar pattern. The rules are simple:

Candle shall be closed in it's upper half

High of this candle shall be below all three Alligator's lines (Jaw, Lips, Teeth)

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

How we can use all these indicators in this strategy? This strategy is a counter trend one. Candle's high shall be below all Alligator's lines. During this market stage the bullish reversal bar candlestick pattern shall be printed. This bar during the downtrend is a high probability setup for the potential reversal to the upside: bulls were able to close the price in the upper half of a candle. The breaking of its high is a high probability signal that trend change is confirmed and script opens long trade. If market continues going down and break down the bullish reversal bar's low potential trend change has been invalidated and strategy close long trade.

If market really reversed and started moving to the upside strategy waits for the trend change form the downtrend to the uptrend according to approximation of Alligator and Fractals combination. If this change happens strategy close the trade. This approach helps to stay in the long trade while the uptrend continuation is likely and close it if there is a high probability of the uptrend finish.

Optionally users can enable MFI and AO filters. First of all, let's briefly explain what are these two indicators. The Awesome Oscillator (AO), created by Bill Williams, is a momentum-based indicator that evaluates market momentum by comparing recent price activity to a broader historical context. It assists traders in identifying potential trend reversals and gauging trend strength.

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

This indicator is filtering signals in the following way: if current AO bar is decreasing this candle can be interpreted as a bullish reversal bar. This logic is applicable because initially this strategy is a trend reversal, it is searching for the high probability setup against the current trend. Decreasing AO is the additional high probability filter of a downtrend.

Let's briefly look what is MFI. The Market Facilitation Index (MFI) is a technical indicator that measures the price movement per unit of volume, helping traders gauge the efficiency of price movement in relation to trading volume. Here's how you can calculate it:

MFI = (High−Low)/Volume

MFI can be used in combination with volume, so we can divide 4 states. Bill Williams introduced these to help traders interpret the interaction between volume and price movement. Here’s a quick summary:

Green Window (Increased MFI & Increased Volume): Indicates strong momentum with both price and volume increasing. Often a sign of trend continuation, as both buying and selling interest are rising.

Fake Window (Increased MFI & Decreased Volume): Shows that price is moving but with lower volume, suggesting weak support for the trend. This can signal a potential end of the current trend.

Squat Window (Decreased MFI & Increased Volume): Shows high volume but little price movement, indicating a tug-of-war between buyers and sellers. This often precedes a breakout as the pressure builds.

Fade Window (Decreased MFI & Decreased Volume): Indicates a lack of interest from both buyers and sellers, leading to lower momentum. This typically happens in range-bound markets and may signal consolidation before a new move.

For our purposes we are interested in squat bars. This is the sign that volume cannot move the price easily. This type of bar increases the probability of trend reversal. In this indicator we added to enable the MFI filter of reversal bars. If potential reversal bar or two preceding bars have squat state this bar can be interpret as a reversal one.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.12.31. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -5.29%

Maximum Single Profit: +29.99%

Net Profit: +5472.66 USDT (+54.73%)

Total Trades: 103 (33.98% win rate)

Profit Factor: 1.634

Maximum Accumulated Loss: 1231.15 USDT (-8.32%)

Average Profit per Trade: 53.13 USDT (+0.94%)

Average Trade Duration: 76 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h ETH/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

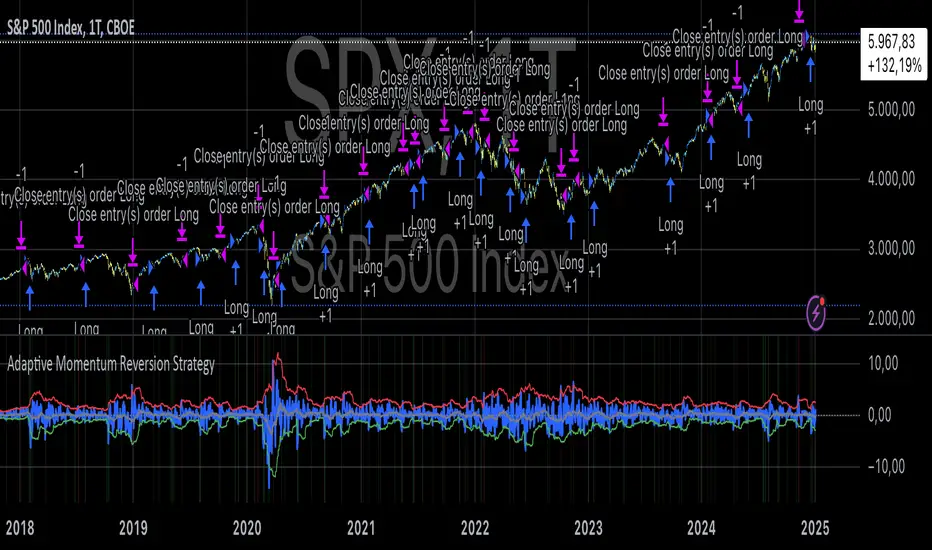

Adaptive Momentum Reversion StrategyThe Adaptive Momentum Reversion Strategy: An Empirical Approach to Market Behavior

The Adaptive Momentum Reversion Strategy seeks to capitalize on market price dynamics by combining concepts from momentum and mean reversion theories. This hybrid approach leverages a Rate of Change (ROC) indicator along with Bollinger Bands to identify overbought and oversold conditions, triggering trades based on the crossing of specific thresholds. The strategy aims to detect momentum shifts and exploit price reversions to their mean.

Theoretical Framework

Momentum and Mean Reversion: Momentum trading assumes that assets with a recent history of strong performance will continue in that direction, while mean reversion suggests that assets tend to return to their historical average over time (Fama & French, 1988; Poterba & Summers, 1988). This strategy incorporates elements of both, looking for periods when momentum is either overextended (and likely to revert) or when the asset’s price is temporarily underpriced relative to its historical trend.

Rate of Change (ROC): The ROC is a straightforward momentum indicator that measures the percentage change in price over a specified period (Wilder, 1978). The strategy calculates the ROC over a 2-period window, making it responsive to short-term price changes. By using ROC, the strategy aims to detect price acceleration and deceleration.

Bollinger Bands: Bollinger Bands are used to identify volatility and potential price extremes, often signaling overbought or oversold conditions. The bands consist of a moving average and two standard deviation bounds that adjust dynamically with price volatility (Bollinger, 2002).

The strategy employs two sets of Bollinger Bands: one for short-term volatility (lower band) and another for longer-term trends (upper band), with different lengths and standard deviation multipliers.

Strategy Construction

Indicator Inputs:

ROC Period: The rate of change is computed over a 2-period window, which provides sensitivity to short-term price fluctuations.

Bollinger Bands:

Lower Band: Calculated with a 18-period length and a standard deviation of 1.7.

Upper Band: Calculated with a 21-period length and a standard deviation of 2.1.

Calculations:

ROC Calculation: The ROC is computed by comparing the current close price to the close price from rocPeriod days ago, expressing it as a percentage.

Bollinger Bands: The strategy calculates both upper and lower Bollinger Bands around the ROC, using a simple moving average as the central basis. The lower Bollinger Band is used as a reference for identifying potential long entry points when the ROC crosses above it, while the upper Bollinger Band serves as a reference for exits, when the ROC crosses below it.

Trading Conditions:

Long Entry: A long position is initiated when the ROC crosses above the lower Bollinger Band, signaling a potential shift from a period of low momentum to an increase in price movement.

Exit Condition: A position is closed when the ROC crosses under the upper Bollinger Band, or when the ROC drops below the lower band again, indicating a reversal or weakening of momentum.

Visual Indicators:

ROC Plot: The ROC is plotted as a line to visualize the momentum direction.

Bollinger Bands: The upper and lower bands, along with their basis (simple moving averages), are plotted to delineate the expected range for the ROC.

Background Color: To enhance decision-making, the strategy colors the background when extreme conditions are detected—green for oversold (ROC below the lower band) and red for overbought (ROC above the upper band), indicating potential reversal zones.

Strategy Performance Considerations

The use of Bollinger Bands in this strategy provides an adaptive framework that adjusts to changing market volatility. When volatility increases, the bands widen, allowing for larger price movements, while during quieter periods, the bands contract, reducing trade signals. This adaptiveness is critical in maintaining strategy effectiveness across different market conditions.

The strategy’s pyramiding setting is disabled (pyramiding=0), ensuring that only one position is taken at a time, which is a conservative risk management approach. Additionally, the strategy includes transaction costs and slippage parameters to account for real-world trading conditions.

Empirical Evidence and Relevance

The combination of momentum and mean reversion has been widely studied and shown to provide profitable opportunities under certain market conditions. Studies such as Jegadeesh and Titman (1993) confirm that momentum strategies tend to work well in trending markets, while mean reversion strategies have been effective during periods of high volatility or after sharp price movements (De Bondt & Thaler, 1985). By integrating both strategies into one system, the Adaptive Momentum Reversion Strategy may be able to capitalize on both trending and reverting market behavior.

Furthermore, research by Chan (1996) on momentum-based trading systems demonstrates that adaptive strategies, which adjust to changes in market volatility, often outperform static strategies, providing a compelling rationale for the use of Bollinger Bands in this context.

Conclusion

The Adaptive Momentum Reversion Strategy provides a robust framework for trading based on the dual concepts of momentum and mean reversion. By using ROC in combination with Bollinger Bands, the strategy is capable of identifying overbought and oversold conditions while adapting to changing market conditions. The use of adaptive indicators ensures that the strategy remains flexible and can perform across different market environments, potentially offering a competitive edge for traders who seek to balance risk and reward in their trading approaches.

References

Bollinger, J. (2002). Bollinger on Bollinger Bands. McGraw-Hill Professional.

Chan, L. K. C. (1996). Momentum, Mean Reversion, and the Cross-Section of Stock Returns. Journal of Finance, 51(5), 1681-1713.

De Bondt, W. F., & Thaler, R. H. (1985). Does the Stock Market Overreact? Journal of Finance, 40(3), 793-805.

Fama, E. F., & French, K. R. (1988). Permanent and Temporary Components of Stock Prices. Journal of Political Economy, 96(2), 246-273.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. Journal of Finance, 48(1), 65-91.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research.

XT Alert Builder - [CrossTrade]The XT Alert Builder is designed to work with CrossTrade and provide an easy way to create strategy entries from Indicator signal sources.

The {{strategy.order.alert_message}} variable along with your Secret Key will send CrossTrade compatible payloads for automated order execution in NinjaTrader 8.

SIGNAL SETTINGS

1. Determine your Entry Signal Source (indicator or OHLC) for both buy and sell signals independently. You can also elect to make the strategy unidirectional by unchecking one of the signal boxes.

2. Determine your Exit Signal Type. The default is Custom which means you're using some kind of input for this like an indicator. Optionally, you can select 'Session End' which will delay the strategy exit until the last bar of the session based n the Trading End Hour/Minute you set in your Trading Hours section.

3. Determine you Exit Sources for Buy and Sells. You can mix and match these inputs for ultimate customization of entries and exits - have fun!

The strategy will by default send a CLOSEPOSITION command to the instrument and account specified based on your Exit settings and time.

TRADING HOURS

Users can specify a trading session or time window to ensure signals only occur during desired hours. The Session End exit signal is based on this window.

NINJATRADER SETTINGS

1. Your NT8 Account. Separate multiple accounts by comma for multi-account placement.

2. Your preferred NT8 instrument in NT compatible format. (e.g. ES 03-25, ES MAR25)

3. Your preferred NT8 quantity

TRADE MANAGEMENT

We've provided both options, you can either use an ATM strategy template or stop loss and take profit levels. More info on Tick and Percentage based stops and targets.

Key Points for successful Trade Management settings application:

1. The ATM template name and qty must match what's saved on Ninja

2. You can choose either ticks or percentage based application - but not both.

3. The stops and target levels need to be offset based on the directional price scale. If you're buying then the stop requires a negative sign and vise versa for Sell orders.

Buy Example:

Take Profit = 50

Stop Loss = -20

CROSSTRADE ADVANCED OPTIONS

Features such as our Flatten first, Require Market Position, Delay Timer, Rate Limiting, and Max Position command enhancements have also been included. More info on these can be found in our Help Docs.

INSTUCTIONS FOR ALERT CREATION

Remove the default info provided by the strategy and then add your CrossTrade secret key and the dynamic strategy variable {{strategy.order.alert_message}}

For example:

Key=your-secret-key;

{{strategy.order.alert_message}}

Trade well,

- CrossTrade Team

three Supertrend EMA Strategy by Prasanna +DhanuThe indicator described in your Pine Script is a Supertrend EMA Strategy that combines the Supertrend and EMA (Exponential Moving Average) to create a trend-following strategy. Here’s a detailed breakdown of how this indicator works:

1. EMA (Exponential Moving Average):

The EMA is a moving average that places more weight on recent prices, making it more responsive to price changes compared to a simple moving average (SMA). In this strategy, the EMA is used to determine the overall trend direction.

Input Parameter:

ema_length: This is the period for the EMA, set to 50 periods by default. A shorter EMA will respond more quickly to price movements, while a longer EMA is smoother and less sensitive to short-term fluctuations.

How it's used:

If the price is above the EMA, it indicates an uptrend.

If the price is below the EMA, it indicates a downtrend.

2. Supertrend Indicator:

The Supertrend indicator is a trend-following tool based on the Average True Range (ATR), which is a volatility measure. It helps to identify the direction of the trend by setting a dynamic support or resistance level.

Input Parameters:

supertrend_atr_period: The period used for calculating the ATR, set to 10 periods by default.

supertrend_multiplier1: Multiplier for the first Supertrend, set to 3.0.

supertrend_multiplier2: Multiplier for the second Supertrend, set to 2.0.

supertrend_multiplier3: Multiplier for the third Supertrend, set to 1.0.

Each Supertrend line has a different multiplier, which affects its sensitivity to price changes. The ATR period defines how many periods of price data are used to calculate the ATR.

How the Supertrend works:

If the Supertrend value is below the price, the trend is considered bullish (uptrend).

If the Supertrend value is above the price, the trend is considered bearish (downtrend).

The Supertrend will switch between up and down based on price movement and ATR, providing a dynamic trend-following signal.

3. Three Supertrend Lines:

In this strategy, three Supertrend lines are calculated with different multipliers and the same ATR period (10 periods). Each line is more or less sensitive to price changes, and they are plotted on the chart in different colors based on whether the trend is bullish (green) or bearish (red).

Supertrend 1: The most sensitive Supertrend with a multiplier of 3.0.

Supertrend 2: A moderately sensitive Supertrend with a multiplier of 2.0.

Supertrend 3: The least sensitive Supertrend with a multiplier of 1.0.

Each Supertrend line signals a bullish trend when its value is below the price and a bearish trend when its value is above the price.

4. Strategy Rules:

This strategy uses the three Supertrend lines combined with the EMA to generate trade signals.

Entry Conditions:

A long entry is triggered when all three Supertrend lines are in an uptrend (i.e., all three Supertrend lines are below the price), and the price is above the EMA. This suggests a strong bullish market condition.

A short entry is triggered when all three Supertrend lines are in a downtrend (i.e., all three Supertrend lines are above the price), and the price is below the EMA. This suggests a strong bearish market condition.

Exit Conditions:

A long exit occurs when the third Supertrend (the least sensitive one) switches to a downtrend (i.e., the price falls below it).

A short exit occurs when the third Supertrend switches to an uptrend (i.e., the price rises above it).

5. Visualization:

The strategy also plots the following on the chart:

The EMA is plotted as a blue line, which helps identify the overall trend.

The three Supertrend lines are plotted with different colors:

Supertrend 1: Green (for uptrend) and Red (for downtrend).

Supertrend 2: Green (for uptrend) and Red (for downtrend).

Supertrend 3: Green (for uptrend) and Red (for downtrend).

Summary of the Strategy:

The strategy combines three Supertrend indicators (with different multipliers) and an EMA to capture both short-term and long-term trends.

Long positions are entered when all three Supertrend lines are bullish and the price is above the EMA.

Short positions are entered when all three Supertrend lines are bearish and the price is below the EMA.

Exits occur when the third Supertrend line (the least sensitive) signals a change in trend direction.

This combination of indicators allows for a robust trend-following strategy that adapts to both short-term volatility and long-term trend direction. The Supertrend lines provide quick reaction to price changes, while the EMA offers a smoother, more stable trend direction for confirmation.

The indicator described in your Pine Script is a Supertrend EMA Strategy that combines the Supertrend and EMA (Exponential Moving Average) to create a trend-following strategy. Here’s a detailed breakdown of how this indicator works:

1. EMA (Exponential Moving Average):

The EMA is a moving average that places more weight on recent prices, making it more responsive to price changes compared to a simple moving average (SMA). In this strategy, the EMA is used to determine the overall trend direction.

Input Parameter:

ema_length: This is the period for the EMA, set to 50 periods by default. A shorter EMA will respond more quickly to price movements, while a longer EMA is smoother and less sensitive to short-term fluctuations.

How it's used:

If the price is above the EMA, it indicates an uptrend.

If the price is below the EMA, it indicates a downtrend.

2. Supertrend Indicator:

The Supertrend indicator is a trend-following tool based on the Average True Range (ATR), which is a volatility measure. It helps to identify the direction of the trend by setting a dynamic support or resistance level.

Input Parameters:

supertrend_atr_period: The period used for calculating the ATR, set to 10 periods by default.

supertrend_multiplier1: Multiplier for the first Supertrend, set to 3.0.

supertrend_multiplier2: Multiplier for the second Supertrend, set to 2.0.

supertrend_multiplier3: Multiplier for the third Supertrend, set to 1.0.

Each Supertrend line has a different multiplier, which affects its sensitivity to price changes. The ATR period defines how many periods of price data are used to calculate the ATR.

How the Supertrend works:

If the Supertrend value is below the price, the trend is considered bullish (uptrend).

If the Supertrend value is above the price, the trend is considered bearish (downtrend).

The Supertrend will switch between up and down based on price movement and ATR, providing a dynamic trend-following signal.

3. Three Supertrend Lines:

In this strategy, three Supertrend lines are calculated with different multipliers and the same ATR period (10 periods). Each line is more or less sensitive to price changes, and they are plotted on the chart in different colors based on whether the trend is bullish (green) or bearish (red).

Supertrend 1: The most sensitive Supertrend with a multiplier of 3.0.

Supertrend 2: A moderately sensitive Supertrend with a multiplier of 2.0.

Supertrend 3: The least sensitive Supertrend with a multiplier of 1.0.

Each Supertrend line signals a bullish trend when its value is below the price and a bearish trend when its value is above the price.

4. Strategy Rules:

This strategy uses the three Supertrend lines combined with the EMA to generate trade signals.

Entry Conditions:

A long entry is triggered when all three Supertrend lines are in an uptrend (i.e., all three Supertrend lines are below the price), and the price is above the EMA. This suggests a strong bullish market condition.

A short entry is triggered when all three Supertrend lines are in a downtrend (i.e., all three Supertrend lines are above the price), and the price is below the EMA. This suggests a strong bearish market condition.

Exit Conditions:

A long exit occurs when the third Supertrend (the least sensitive one) switches to a downtrend (i.e., the price falls below it).

A short exit occurs when the third Supertrend switches to an uptrend (i.e., the price rises above it).

5. Visualization:

The strategy also plots the following on the chart:

The EMA is plotted as a blue line, which helps identify the overall trend.

The three Supertrend lines are plotted with different colors:

Supertrend 1: Green (for uptrend) and Red (for downtrend).

Supertrend 2: Green (for uptrend) and Red (for downtrend).

Supertrend 3: Green (for uptrend) and Red (for downtrend).

Summary of the Strategy:

The strategy combines three Supertrend indicators (with different multipliers) and an EMA to capture both short-term and long-term trends.

Long positions are entered when all three Supertrend lines are bullish and the price is above the EMA.

Short positions are entered when all three Supertrend lines are bearish and the price is below the EMA.

Exits occur when the third Supertrend line (the least sensitive) signals a change in trend direction.

This combination of indicators allows for a robust trend-following strategy that adapts to both short-term volatility and long-term trend direction. The Supertrend lines provide quick reaction to price changes, while the EMA offers a smoother, more stable trend direction for confirmation.

The indicator described in your Pine Script is a Supertrend EMA Strategy that combines the Supertrend and EMA (Exponential Moving Average) to create a trend-following strategy. Here’s a detailed breakdown of how this indicator works:

1. EMA (Exponential Moving Average):

The EMA is a moving average that places more weight on recent prices, making it more responsive to price changes compared to a simple moving average (SMA). In this strategy, the EMA is used to determine the overall trend direction.

Input Parameter:

ema_length: This is the period for the EMA, set to 50 periods by default. A shorter EMA will respond more quickly to price movements, while a longer EMA is smoother and less sensitive to short-term fluctuations.

How it's used:

If the price is above the EMA, it indicates an uptrend.

If the price is below the EMA, it indicates a downtrend.

2. Supertrend Indicator:

The Supertrend indicator is a trend-following tool based on the Average True Range (ATR), which is a volatility measure. It helps to identify the direction of the trend by setting a dynamic support or resistance level.

Input Parameters:

supertrend_atr_period: The period used for calculating the ATR, set to 10 periods by default.

supertrend_multiplier1: Multiplier for the first Supertrend, set to 3.0.

supertrend_multiplier2: Multiplier for the second Supertrend, set to 2.0.

supertrend_multiplier3: Multiplier for the third Supertrend, set to 1.0.

Each Supertrend line has a different multiplier, which affects its sensitivity to price changes. The ATR period defines how many periods of price data are used to calculate the ATR.

How the Supertrend works:

If the Supertrend value is below the price, the trend is considered bullish (uptrend).

If the Supertrend value is above the price, the trend is considered bearish (downtrend).

The Supertrend will switch between up and down based on price movement and ATR, providing a dynamic trend-following signal.

3. Three Supertrend Lines:

In this strategy, three Supertrend lines are calculated with different multipliers and the same ATR period (10 periods). Each line is more or less sensitive to price changes, and they are plotted on the chart in different colors based on whether the trend is bullish (green) or bearish (red).

Supertrend 1: The most sensitive Supertrend with a multiplier of 3.0.

Supertrend 2: A moderately sensitive Supertrend with a multiplier of 2.0.

Supertrend 3: The least sensitive Supertrend with a multiplier of 1.0.

Each Supertrend line signals a bullish trend when its value is below the price and a bearish trend when its value is above the price.

4. Strategy Rules:

This strategy uses the three Supertrend lines combined with the EMA to generate trade signals.

Entry Conditions:

A long entry is triggered when all three Supertrend lines are in an uptrend (i.e., all three Supertrend lines are below the price), and the price is above the EMA. This suggests a strong bullish market condition.

A short entry is triggered when all three Supertrend lines are in a downtrend (i.e., all three Supertrend lines are above the price), and the price is below the EMA. This suggests a strong bearish market condition.

Exit Conditions:

A long exit occurs when the third Supertrend (the least sensitive one) switches to a downtrend (i.e., the price falls below it).

A short exit occurs when the third Supertrend switches to an uptrend (i.e., the price rises above it).

5. Visualization:

The strategy also plots the following on the chart:

The EMA is plotted as a blue line, which helps identify the overall trend.

The three Supertrend lines are plotted with different colors:

Supertrend 1: Green (for uptrend) and Red (for downtrend).

Supertrend 2: Green (for uptrend) and Red (for downtrend).

Supertrend 3: Green (for uptrend) and Red (for downtrend).

Summary of the Strategy:

The strategy combines three Supertrend indicators (with different multipliers) and an EMA to capture both short-term and long-term trends.

Long positions are entered when all three Supertrend lines are bullish and the price is above the EMA.

Short positions are entered when all three Supertrend lines are bearish and the price is below the EMA.

Exits occur when the third Supertrend line (the least sensitive) signals a change in trend direction.

This combination of indicators allows for a robust trend-following strategy that adapts to both short-term volatility and long-term trend direction. The Supertrend lines provide quick reaction to price changes, while the EMA offers a smoother, more stable trend direction for confirmation.

Custom Strategy: ETH Martingale 2.0Strategic characteristics

ETH Little Martin 2.0 is a self-developed trading strategy based on the Martingale strategy, mainly used for trading ETH (Ethereum). The core idea of this strategy is to place orders in the same direction at a fixed price interval, and then use Martin's multiple investment principle to reduce losses, but this is also the main source of losses.

Parameter description:

1 Interval: The minimum spacing for taking profit, stop loss, and opening/closing of orders. Different targets have different spacing. Taking ETH as an example, it is generally recommended to have a spacing of 2% for fluctuations in the target.

2 Base Price: This is the price at which you triggered the first order. Similarly, I am using ETH as an example. If you have other targets, I suggest using the initial value of a price that can be backtesting. The Base Price is only an initial order price and has no impact on subsequent orders.

3 Initial Order Amount: Users can set an initial order amount to control the risk of each transaction. If the stop loss is reached, we will double the amount based on this value. This refers to the value of the position held, not the number of positions held.

4 Loss Multiplier: The strategy will increase the next order amount based on the set multiple after the stop loss, in order to make up for the previous losses through a larger position. Note that after taking profit, it will be reset to 1 times the Initial Order Amount.

5. Long Short Operation: The first order of the strategy is a multiple entry, and in subsequent orders, if the stop loss is reached, a reverse order will be opened. The position value of a one-way order is based on the Loss Multiplier multiple investment, so it is generally recommended that the Loss Multiplier default to 2.

Improvement direction

Although this strategy already has a certain trading logic, there are still some improvement directions that can be considered:

1. Dynamic adjustment of spacing: Currently, the spacing is fixed, and it can be considered to dynamically adjust the spacing based on market volatility to improve the adaptability of the strategy. Try using dynamic spacing, which may be more suitable for the actual market situation.

2. Filtering criteria: Orders and no orders can be optimized separately. The biggest problem with this strategy is that it will result in continuous losses during fluctuations, and eventually increase the investment amount. You can consider filtering out some fluctuations or only focusing on trend trends.

3. Risk management: Add more risk management measures, such as setting a maximum loss limit to avoid huge losses caused by continuous stop loss.

4. Optimize the stop loss multiple: Currently, the stop loss multiple is fixed, and it can be considered to dynamically adjust the multiple according to market conditions to reduce risk.

Liquid Pours XtremeStrategy Description: Liquid Pours Xtreme

The Liquid Pours Xtreme is an innovative trading strategy that combines the analysis of specific time-based patterns with price comparisons to identify potential opportunities in the forex market. Designed for traders seeking a structured methodology based on clear rules, this strategy offers integration with Telegram for real-time alerts and provides visual tools to enhance trade management.

Key Features:

Analysis of Specific Time Patterns: The strategy captures and compares closing prices at two key moments during the trading day, identifying recurring patterns that may indicate future market movements.

Dynamic SL and TP Levels Implementation: Utilizes tick-based calculations to set Stop-Loss and Take-Profit levels, adapting to the current market volatility.

Advanced Telegram Integration: Provides detailed alerts including information such as the asset, signal time, entry price, and SL/TP levels, facilitating real-time decision-making.

Complete Customization: Allows users to adjust key parameters, including operation schedules, weekdays, and visual settings, adapting to different trading styles.

Enhanced Chart Visualization: Includes visual elements like candle color changes based on signal state, event markers, and halos to highlight important moments.

Default Strategy Properties: Specific configuration for optimal risk management and simulation.

How the Strategy Works

Capturing Prices at Key Moments:

- The strategy records the closing price at two user-defined specific times. These times typically correspond to periods of high market volatility, such as the opening of the European session and the US pre-market.

- Rationale: Volatility and trading volume usually increase during these times, presenting opportunities for significant price movements.

Generating Signals Based on Price Comparison:

- Buy Signal: If the second closing price is lower than the first, it indicates possible accumulation and is interpreted as a bullish signal.

- Sell Signal: If the second closing price is higher than the first, it suggests possible distribution and is interpreted as a bearish signal.

- Signals are only generated on selected trading days, allowing you to avoid days with lower liquidity or higher risk.

Calculating Dynamic SL and TP Levels:

- Stop-Loss (SL) and Take-Profit (TP) levels are calculated based on the entry price and a user-defined number of ticks, adapting to market volatility.

- The strategy offers the option to base these levels on the close of the signal candle or the open of the next candle, providing flexibility according to the trader's preference.

- SL and TP boxes are drawn on the chart for visual reference, facilitating trade management.

Automatic Execution and Alerts:

- Upon signal generation, the strategy automatically executes a market order (buy or sell).

- Sends a detailed alert to your Telegram channel, including essential information for quick decision-making.

Visual Elements:

- Colors candles based on the signal state: buy, sell, or neutral, allowing for quick trend identification.

- Provides a smooth color transition between signal states and uses markers and halos to highlight important events and signals on the chart.

Trade Management:

- Manages open trades with automatic exit conditions based on the established SL and TP levels.

- Includes mechanisms to prevent exceeding TradingView's limitations on boxes and labels, ensuring optimal script performance.

Originality and utility:

- This strategy incorporates a unique approach focusing on specific time patterns and their relationship to institutional activity in the market.

How to Use the Strategy

Add the Script to the Chart:

- Go to the indicators menu in TradingView.

- Search for " Liquid Pours Xtreme " and add it to your chart.

Set Up Telegram Alerts:

- Enter your Telegram Chat ID in the script parameters to receive alerts.

- Customize the Buy and Sell alert messages as desired.

Configure Time Patterns:

- Set the hours and minutes for the two times you want to compare closing prices, aligning them with relevant market sessions or events.

Set SL and TP Parameters:

- Define the number of ticks for the Stop-Loss and Take-Profit levels, adapting them to the asset you're trading and your risk tolerance.

- Choose the basis for SL and TP calculation (close of the signal candle or open of the next candle).

Select Trading Days:

- Enable or disable trading on specific days of the week, allowing you to avoid days with lower activity or unexpected volatility.

Customize Visual Elements:

- Adjust the colors and styles of visual elements to enhance readability and suit your personal preferences.

Monitor the Strategy:

- Observe the chart for signals and use Telegram alerts to stay informed of new opportunities, even when you're not at your terminal.

Testing and Optimization:

- Use TradingView's backtesting features to evaluate the historical performance of the strategy with different parameters.

- Adjust and optimize the parameters based on the results and your own analysis.

Adjust the Strategy Properties:

- Ensure that the strategy properties (order size, commission, slippage) are aligned with your trading account and platform to obtain realistic results.

Strategy Properties (Important)

This script backtest is conducted on M30 EURUSD , using the following backtesting properties:

Initial Capital: $10,000

Order Size: 50,000 Contracts (equivalent to 0.5% of the capital)

Commission: $0.20 per order

Slippage: 1 tick

Pyramiding: 1 order

Verify Price for Limit Orders: 0 ticks

Recalculate on Order Execution: Enabled

Recalculate on Every Tick: Enabled

Recalculate After Order Filled: Enabled

Bar Magnifier for Backtesting Precision: Enabled

We use these properties to ensure a realistic preview of the backtesting system. Note that default properties may vary for different reasons:

- Order Size: It is essential to calculate the contract size according to the traded asset and desired risk level.

- Commission and Slippage: These costs can vary depending on the market and instrument; there is no default value that might return realistic results.

We strongly recommend all users adjust the Properties within the script settings to align with their accounts and trading platforms to ensure the results from the strategies are realistic.

Backtesting Results:

- Net Profit: $4,037.50 (40.37%)

- Total Closed Trades : 292

- Profitability Percentage: 26.71%

- Profit Factor: 1.369

- Max Drawdown: $769.30 (6.28%)

- Average Trade: $13.83 (0.03%)

- Average Bars in Trades: 11

These results were obtained under the mentioned conditions and properties, providing an overview of the strategy's historical performance.

Interpreting Results:

- The strategy has demonstrated profitability in the analyzed period, although with a win rate of 26.71%, indicating that success relies on a favorable risk-reward ratio.

- The profit factor of 1.369 suggests that total gains exceed total losses by that proportion.

- It is crucial to consider the maximum drawdown of 6.28% when evaluating the strategy's suitability to your risk tolerance.

Risk Warning:

Trading leveraged financial instruments carries a high level of risk and may not be suitable for all investors. Before deciding to trade, you should carefully consider your investment objectives, level of experience, and risk tolerance. Past performance does not guarantee future results. It is essential to conduct additional testing and adjust the strategy according to your needs.

---

What Makes This Strategy Original?

Time-Based Pattern Approach: Unlike conventional strategies, this strategy focuses on identifying time patterns that reflect institutional activity and macroeconomic events that can influence the market.

Advanced Technological Integration: The combination of automatic execution and customized alerts via Telegram provides an efficient and modern tool for active traders.

Customization and Adaptability: The wide range of adjustable parameters allows the strategy to be tailored to different assets, time zones, and trading styles.

Enhanced Visual Tools: Incorporated visual elements facilitate quick market interpretation and informed decision-making.

Additional Considerations

Continuous Testing and Optimization: Users are encouraged to perform additional backtesting and optimize parameters according to their own observations and requirements.

Complementary Analysis: Use this strategy in conjunction with other indicators and fundamental analysis to reinforce decision-making.

Rigorous Risk Management: Ensure that SL and TP levels, as well as position sizing, align with your risk management plan.

Updates and Support: I am committed to providing updates and improvements based on community feedback. For inquiries or suggestions, feel free to contact me.

---

Example Configuration

Assuming you want to use the strategy with the following parameters:

Telegram Chat ID: Your unique Telegram Chat ID

First Time (Hour:Minute): 6:30

Second Time (Hour:Minute): 7:30

SL Ticks: 100

TP Ticks: 400

SL and TP Basis: Close of the Signal Candle

Trading Days: Tuesday, Wednesday, Thursday

Simulated Initial Capital: $10,000

Risk per Trade in Simulation: $50 (-0.5% of capital)

Slippage and Commissions in Simulation: 1 tick of slippage and $0.20 commission per trade

---

Conclusion

The Liquid Pours Xtreme strategy offers an innovative approach by combining specific time analysis with robust risk management and modern technological tools. Its original and adaptable design makes it valuable for traders looking to diversify their methods and capitalize on opportunities based on less conventional patterns.

Ready for immediate implementation in TradingView, this strategy can enrich your trading arsenal and contribute to a more informed and structured approach to your operations.

---

Final Disclaimer:

Financial markets are volatile and can present significant risks. This strategy should be used as part of a comprehensive trading approach and does not guarantee positive results. It is always advisable to consult with a professional financial advisor before making investment decisions.

---

Bollinger Breakout Strategy with Direction Control [4H crypto]Bollinger Breakout Strategy with Direction Control - User Guide

This strategy leverages Bollinger Bands, RSI, and directional filters to identify potential breakout trading opportunities. It is designed for traders looking to capitalize on significant price movements while maintaining control over trade direction (long, short, or both). Here’s how to use this strategy effectively:

How the Strategy Works

Indicators Used:

Bollinger Bands:

A volatility-based indicator with an upper and lower band around a simple moving average (SMA). The bands expand or contract based on market volatility.

RSI (Relative Strength Index):

Measures momentum to determine overbought or oversold conditions. In this strategy, RSI is used to confirm breakout strength.

Trade Direction Control:

You can select whether to trade:

Long only: Buy positions.

Short only: Sell positions.

Both: Trade in both directions depending on conditions.

Breakout Conditions:

Long Trade:

The price closes above the upper Bollinger Band.

RSI is above the midline (50), confirming upward momentum.

The "Trade Direction" setting allows either "Long" or "Both."

Short Trade:

The price closes below the lower Bollinger Band.

RSI is below the midline (50), confirming downward momentum.

The "Trade Direction" setting allows either "Short" or "Both."

Risk Management:

Stop-Loss:

Long trades: Set at 2% below the entry price.

Short trades: Set at 2% above the entry price.

Take-Profit:

Calculated using a Risk/Reward Ratio (default is 2:1).

Adjust this in the strategy settings.

Inputs and Customization

Key Parameters:

Bollinger Bands Length: Default is 20. Adjust based on the desired sensitivity.

Multiplier: Default is 2.0. Higher values widen the bands; lower values narrow them.

RSI Length: Default is 14, which is standard for RSI.

Risk/Reward Ratio: Default is 2.0. Increase for more aggressive profit targets, decrease for conservative exits.

Trade Direction:

Options: "Long," "Short," or "Both."

Example: Set to "Long" in a bullish market to focus only on buy trades.

How to Use This Strategy

Adding the Strategy:

Paste the script into TradingView’s Pine Editor and add it to your chart.

Setting Parameters:

Adjust the Bollinger Band settings, RSI, and Risk/Reward Ratio to fit the asset and timeframe you're trading.

Analyzing Signals:

Green line (Upper Band): Signals breakout potential for long trades.

Red line (Lower Band): Signals breakout potential for short trades.

Blue line (Basis): Central Bollinger Band (SMA), helpful for understanding price trends.

Testing the Strategy:

Use the Strategy Tester in TradingView to backtest performance on your chosen asset and timeframe.

Optimizing for Assets:

Forex pairs, cryptocurrencies (like BTC), or stocks with high volatility are ideal for this strategy.

Works best on higher timeframes like 4H or Daily.

Best Practices

Combine with Volume: Confirm breakouts with increased volume for higher reliability.

Avoid Sideways Markets: Use additional trend filters (like ADX) to avoid trades in low-volatility conditions.

Optimize Parameters: Regularly adjust the Bollinger Bands multiplier and RSI settings to match the asset's behavior.

By utilizing this strategy, you can effectively trade breakouts while maintaining flexibility in trade direction. Adjust the parameters to match your trading style and market conditions for optimal results!

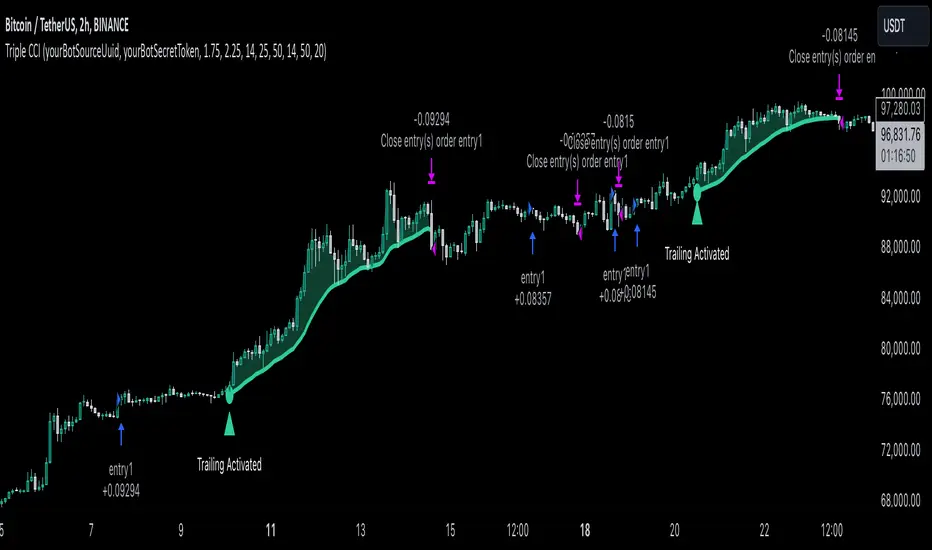

Triple CCI Strategy MFI Confirmed [Skyrexio]Overview

Triple CCI Strategy MFI Confirmed leverages 3 different periods Commodity Channel Index (CCI) indicator in conjunction Money Flow Index (MFI) and Exponential Moving Average (EMA) to obtain the high probability setups. Fast period CCI is used for having the high probability to enter in the direction of short term trend, middle and slow period CCI are used for confirmation, if market now likely in the mid and long-term uptrend. MFI is used to confirm trade with the money inflow/outflow with the high probability. EMA is used as an additional trend filter. Moreover, strategy uses exponential moving average (EMA) to trail the price when it reaches the specific level. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Four layers trade filtering system: Strategy utilizes two different period CCI indicators, MFI and EMA indicators to confirm the signals produced by fast period CCI.

Trailing take profit level: After reaching the trailing profit activation level scrip activate the trailing of long trade using EMA. More information in methodology.

Methodology

The strategy opens long trade when the following price met the conditions:

Fast period CCI shall crossover the zero-line.

Slow and Middle period CCI shall be above zero-lines.

Price shall close above the EMA. Crossover is not obligatory

MFI shall be above 50

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with EMA. If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.75)

ATR Trailing Profit Activation Level (by default = 2.25)

CCI Fast Length (by default = 14, used for calculation short term period CCI)

CCI Middle Length (by default = 25, used for calculation short term period CCI)

CCI Slow Length (by default = 50, used for calculation long term period CCI)

MFI Length (by default = 14, used for calculation MFI

EMA Length (by default = 50, period of EMA, used for trend filtering EMA calculation)

Trailing EMA Length (by default = 20)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is CCI, MFI and EMA.

The Commodity Channel Index (CCI) is a momentum-based technical indicator that measures the deviation of a security's price from its average price over a specific period. It helps traders identify overbought or oversold conditions and potential trend reversals.

The CCI formula is:

CCI = (Typical Price − SMA) / (0.015 × Mean Deviation)

Typical Price (TP): This is calculated as the average of the high, low, and closing prices for the period.

Simple Moving Average (SMA): This is the average of the Typical Prices over a specific number of periods.

Mean Deviation: This is the average of the absolute differences between the Typical Price and the SMA.

The result is a value that typically fluctuates between +100 and -100, though it is not bounded and can go higher or lower depending on the price movement.

The Money Flow Index (MFI) is a technical indicator that measures the strength of money flowing into and out of a security. It combines price and volume data to assess buying and selling pressure and is often used to identify overbought or oversold conditions. The formula for MFI involves several steps:

1. Calculate the Typical Price (TP):

TP = (high + low + close) / 3

2. Calculate the Raw Money Flow (RMF):

Raw Money Flow = TP × Volume

3. Determine Positive and Negative Money Flow:

If the current TP is greater than the previous TP, it's Positive Money Flow.

If the current TP is less than the previous TP, it's Negative Money Flow.

4. Calculate the Money Flow Ratio (MFR):

Money Flow Ratio = Sum of Positive Money Flow (over n periods) / Sum of Negative Money Flow (over n periods)

5. Calculate the Money Flow Index (MFI):

MFI = 100 − (100 / (1 + Money Flow Ratio))

MFI above 80 can be considered as overbought, below 20 - oversold.

The Exponential Moving Average (EMA) is a type of moving average that places greater weight and significance on the most recent data points. It is widely used in technical analysis to smooth price data and identify trends more quickly than the Simple Moving Average (SMA).

Formula:

1. Calculate the multiplier

Multiplier = 2 / (n + 1) , Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

This strategy leverages Fast period CCI, which shall break the zero line to the upside to say that probability of short term trend change to the upside increased. This zero line crossover shall be confirmed by the Middle and Slow periods CCI Indicators. At the moment of breakout these two CCIs shall be above 0, indicating that there is a high probability that price is in middle and long term uptrend. This approach increases chances to have a long trade setup in the direction of mid-term and long-term trends when the short-term trend starts to reverse to the upside.

Additionally strategy uses MFI to have a greater probability that fast CCI breakout is confirmed by this indicator. We consider the values of MFI above 50 as a higher probability that trend change from downtrend to the uptrend is real. Script opens long trades only if MFI is above 50. As you already know from the MFI description, it incorporates volume in its calculation, therefore we have another one confirmation factor.

Finally, strategy uses EMA an additional trend filter. It allows to open long trades only if price close above EMA (by default 50 period). It increases the probability of taking long trades only in the direction of the trend.